The market had every reason to break. It didn’t. Here’s what that means.

They say the market is the most brutal editor of investment theses. Right now, it’s doing exactly that to mine.

In my last two posts, I laid out a case: extreme valuations, geopolitical risk, AI bubble parallels, and an inflationary shock that would weigh heavily on equities. The analysis wasn’t wrong—it still isn’t. But here’s the humbling truth after 35+ years in markets: being right about the fundamentals and being right about the trade are two very different things. Price action doesn’t lie. And right now, it’s telling a very different story.

The Oil Signal That Changed Everything

Let me start with what really got my attention—and it wasn’t just oil. The SPX did break down below that key 6,550 support level I flagged. In fact it went further, trading down to 6,390. Blink and you missed it. Almost immediately, the market staged one of the most violent rallies I’ve seen since the tariff tantrum—and it traded straight back through 6,550 and beyond. Now, the consensus among market commentators was predictable: classic dead cat bounce, next leg lower is coming, use the rally to sell. That was the narrative. That was the “smart” trade.

But here’s where I stopped and asked myself a different question.

Because at the exact same time, oil—which had every reason to be trading at $200 given a genuine war in the Middle East and disruption to the Strait of Hormuz—had topped out around $120 and was struggling to hold even that. Two markets. Two completely different stories from what the fundamentals said should be happening.

When price refuses to confirm the narrative, you have to stop and ask: is the narrative wrong, or is it already fully priced? In this case, I think the answer is both. The bears had their shot. The SPX broke support, printed 6,390, and the sellers couldn’t hold it. Oil had the most bullish fundamental backdrop in years and couldn’t sustain $120. The market absorbed a genuine war, supply disruption fears, and a 50%+ spike in crude—and not only did equities not collapse, they ripped higher off the lows.

That’s not weakness. That’s resilience. And when the worst headlines in years can’t break a market—when it shrugs off what should have been devastating—that’s one of the oldest bullish signals in the book.

Updating the View: The Blow-Off Top Is Back On

I’ll own it. Three weeks ago I was starting to walk away from the blow-off top thesis. The SPX breaking support at 6,550, five months of range-bound price action, and deteriorating macro conditions had me leaning toward something more sinister.

I’m walking that back.

Price action has a habit of making fools of even the most well-reasoned views—including mine. What I’m now seeing is a market that has digested significant headwinds and is beginning to coil again. When you combine what the oil market is signalling with the technical setup re-emerging, the probability weighting shifts.

My original thesis—a blow-off top toward 7,500 on the SPX—looks more likely today than it did a month ago. Brave? Probably. Stupid? Maybe. But if there’s one lesson that’s been drilled into me across 35 years of trading bonds, currencies, equities, and derivatives with leverage: don’t marry your views. When price speaks, listen.

The Global Economy: Resilient, But Diverging Fast

The macro backdrop, while increasingly complex, offers more support for the blow-off top thesis than the bears would like to admit.

The US economy remains the standout — and the political backdrop is about to get more interesting. The “Big Beautiful Bill” — Trump’s sweeping tax and spending package — is already injecting fiscal stimulus at a scale that keeps growth well-supported. Add America’s position as a net energy exporter, effectively oil self-sufficient, and you have an economy genuinely insulated from the supply shock squeezing everyone else.

But here’s what I think the market isn’t fully pricing yet. Trump is due to visit China within the next month — and if I know anything about how he operates, he’s going in to win. He needs a deal. He needs a headline. With midterms on the horizon, the last thing Trump can afford is to drift toward lame duck status, and he knows it. In my view, he will throw everything at this — trade concessions, optics, bilateral frameworks, whatever it takes to come home with something that looks like a win. A Trump-China thaw, even a partial one, could unleash another wave of optimism in markets that are already looking for reasons to run.

Layer on top of that the fiscal reality: a president fighting for legacy and relevance before midterms means more spending, not less. That’s more stimulus, more liquidity, more fuel for the blow-off top I’m calling.

Analyst earnings forecasts for the S&P 500 have already been revised significantly higher — well above what current valuations would suggest — and if those numbers hold, the valuation argument becomes considerably less alarming. The Washington narrative is familiar: any inflation from tariffs and energy is transitory, absorbed by a resilient consumer and a strong labour market. We’ve heard this story before. But in the near term, the market is willing to buy it — and markets move on narratives, at least until they don’t.

China Silence?

China is the other piece of this puzzle. Growth is still tracking around 5% GDP—a number many Western economists quietly don’t believe, but one the market trades off. What’s genuinely underappreciated is how structurally insulated China has made itself from the oil shock. Preferential access to Russian crude at discounted prices, and potentially Iranian supply through back channels, means Beijing is largely bypassing the geopolitical premium the rest of the world is paying at the pump. That’s a meaningful competitive buffer—and it keeps Chinese industrial activity humming while others are squeezed.

The rest of Asia is a very different story. Outside of China, the region looks genuinely vulnerable. Japan, South Korea, India, and most of Southeast Asia remain heavily import-dependent for energy. Elevated oil prices flow directly into inflation, currency pressure, and deteriorating current accounts. If this oil shock persists, Asia ex-China is where the macro pain will be most acutely felt—and where the next round of risk-off pressure could originate.

What About Australia?

Let me be direct. Despite everything I’ve said about the blow-off top and near-term equity resilience, I remain super bearish on the Australian economy—and Australia is not USA or China and sadly I cant get too excited about our ASX 200.

The RBA has moved once so far, with another 0.25% hike all but locked in for early May. With employment still solid, there’s no economic pressure forcing the board to hold. A stable labour market gives them cover to keep tightening, and they’ll use it.

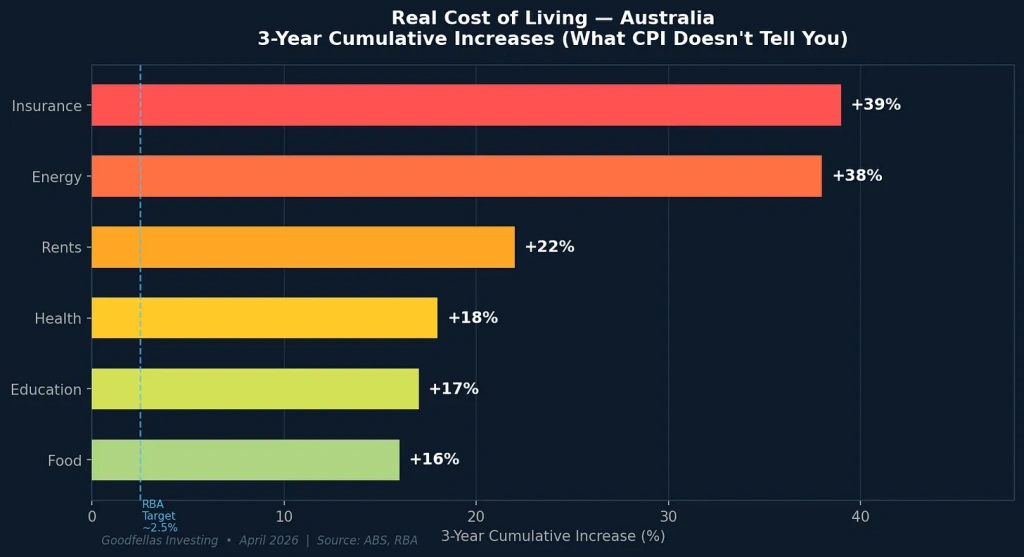

What makes this particularly painful is that higher interest rates are feeding back into an inflationary backdrop already embedded in the real economy—one that, in my view, is grossly underreported in the official data. On paper, CPI looks contained. In reality, anyone filling a supermarket trolley, opening a power bill, or renewing a lease knows the true cost of living over the past three years tells a very different story.

These aren’t abstract line items in a government report—they’re the bills landing in every Australian letterbox, every single month. The result? Consumer confidence is lower today than it was during COVID. Let that sink in. During a global pandemic—when people were locked in their homes and the economy was literally shut down—Australians felt more financially secure than they do right now. That gap between the official narrative and lived reality is the story the RBA can’t ignore forever.

But it Gets Worse for the Little Aussie Battler

While the world debates when oil prices might fall, Australia faces a far more immediate problem that’s being widely ignored — and it’s genuinely alarming.

Australia holds around 30 days of diesel supply, not the 90 days required under IEA rules. We’re the only IEA member that has consistently failed to meet this obligation for more than a decade. By any serious standard, our energy security buffer is dangerously thin.

The supply side is just as fragile. In 2005, Australia had eight operating refineries. Today, we have two — covering barely 20% of national fuel demand. The rest is imported. That leaves us at the very end of global supply chains, precisely when disruptions are becoming more frequent.

Then there’s demand. Australia consumes 7.7 barrels of diesel per person each year, the highest of any major economy. We are the most diesel‑dependent economy on the planet — and we have just 30 days of it. An extended interruption would hit transport, agriculture, mining, construction and food distribution almost immediately.

Fuel rationing is no longer a fringe idea — it’s now a real policy risk. Even partial rationing would have fast and severe economic consequences: freight costs surge, food prices rise, construction stalls, mining output falls, and the cost-of-living shock would dwarf anything caused by recent RBA rate hikes. That isn’t alarmism — it’s simple arithmetic.

Which brings me to the end game. Rate hikes are blunt instruments—they work slowly, quietly, doing what they always do: draining demand, compressing margins, and tightening the screws on households already stretched by three years of cumulative cost increases. Add one more hike on top of this, and the weight of this tightening cycle will eventually crack something. The economy will buckle. It always does.

My call: rate cuts by the end of 2026, or into early 2027. When that pivot comes, it will likely be faster and deeper than the market currently expects. That’s when the genuinely interesting opportunity in rate-sensitive assets opens up. Stay patient.

What I’m Watching and Buying

If we do get the move I’m now expecting, the opportunity set is tilted heavily toward the US. Frankly, there’s less to get excited about on the ASX right now — the pickings are thinner and the growth runway shorter. But for those wanting direct Australian exposure, there are a handful of beaten-down names worth watching. The real action, in my view, is in high-growth US assets positioned to run hard if the blow-off top plays out.

Xero – It has a regulatory moat

After a 60%+ selloff, the conversation has become far more interesting. Xero remains a best-in-class SaaS platform serving SMEs across Australia, New Zealand, and the UK. The selloff wasn’t about the business breaking—it was driven by a sharp sentiment shift following the launch of Claude’s Cowork AI agents, capable of executing multi-step workflows autonomously, which sparked broader fears around SaaS disintermediation. The market sold first and asked questions later.

Here’s what’s interesting though. Even after analysts trimmed their price targets—with recent downgrades landing around $125—there is still roughly 75% upside from current levels to reach that target. Let that number sit for a moment. This isn’t a speculative punt on an unproven business; this is a profitable, cash-generative platform with deep switching costs and a loyal SME customer base, and the market is pricing it like the business model is broken. It isn’t. The AI disruption fear is real, but it’s been extrapolated well beyond what the near-term evidence supports.

Imricor – Still My Highest Conviction Position

Regular readers know Imricor is a constant in these posts — I’ve held since around 30 cents, it’s near $2.00 today, and I haven’t sold a share. Two recent announcements worth highlighting.

The VISABL-VT trial has added a third major European hospital, with world-class electrophysiologists now on board across Prague, Berlin, and Amsterdam. Leading centres don’t sign up for trials they don’t believe in — that’s a meaningful signal.

But the announcement I’m most excited about is NorthStar. Imricor has submitted its NorthStar cardiac mapping system to the FDA to expand its label into paediatric use — and this is where it gets really interesting. Children’s hospitals have been knocking on the door. Why? Because MRI-guided procedures eliminate radiation exposure — something that matters enormously when your patient is a child. The FDA recently cleared NorthStar in adults, and this paediatric submission follows directly from that momentum.

Think about what this means practically. If cleared, Imricor has a near-term, real-world pathway to build an installed base in the US, generate revenue, and get its platform in front of hospital networks — ahead of the broader adult rollout. It’s a foot in the door of the world’s most important medical device market, through one of the most compelling use cases imaginable.

This is a company opening multiple doors at once — clinically, geographically, commercially. No single binary bet. No waiting for one big approval and hoping. Just methodical, compounding progress. Analyst targets still point to substantial upside from here, and with key FDA decisions still pending, the best of this story may still be ahead. I’m not moving.

Technically, the chart is telling an interesting story too. The previous high was $1.83, and since then a significant amount of price action has been consolidating between $1.80 and $2.00 — exactly the kind of base-building behaviour you want to see before a sustained move higher. When a stock grinds sideways in a tight range above a key previous high rather than selling off, it’s absorbing supply and coiling. It wouldn’t surprise me at all to see $2.50 by June 30. That’s not wishful thinking — that’s what the chart is setting up.

Bitcoin

Looks to me like Bitcoin made a meaningful low over the past two months. The washout toward $55,000 I flagged as a risk appears to have played out. The risk-reward is shifting back to the bulls—I can see this returning to triple digits and beyond. The long-term thesis hasn’t changed: generational adoption, digital scarcity, and an institutional buyer base that barely existed five years ago.

Robotics

Still a theme I like. The selloff has created genuine value in a sector with decade-long structural tailwinds. Not adding aggressively, but certainly not selling.

Nuclear Energy

Down here, nuclear looks compelling. The energy transition narrative has been chaotic—but the physics hasn’t changed. Nuclear remains the only scalable, reliable, zero-emission baseload power source. At current valuations, quality uranium and nuclear infrastructure names offer an asymmetric opportunity for patient capital.

The next AI growth theme is agentic AI.

For the past 18 months, AI investing has focused on the inputs — chips, data centres, and the huge cost of building models. The next phase is different. It’s about what those models can actually do.

The first wave of AI was reactive. You asked a question and got an answer. Helpful, but you still did the work. Agentic AI goes further — it can plan, decide, and complete multi‑step tasks on its own. The difference is simple: one answers questions, the other takes action.

What really matters are the agentic utilities — the infrastructure companies that make this possible. These platforms automate entire workflows, from customer support and compliance to invoicing and supply chains, with minimal human input. Once embedded, they’re hard to replace.

This is where I see the most durable returns in AI: not in model builders spending heavily to stay ahead, but in the quiet utility‑layer businesses becoming essential to how work gets done. This is where I’ll be focusing for the next opportunity.

Closing: Stay Humble, But Stay in the Game

Markets humiliate the overconfident and reward the adaptable. I’ve updated my view — not because the fundamentals improved, but because price action is the ultimate arbiter, and right now it’s telling me to lean in.

The risks haven’t disappeared. But when the worst headlines can’t break a market, you have to respect what that’s saying.

A reminder on how I invest: my time horizon is 3 to 7 years. I’m not trading the next headline — I’m positioning for what forms on the other side of uncertainty. That’s where the real money is made.

Until next time—safe investing, and as always, feel free to share with friends and family.