And the Goverment wants a thank you note! (Reading time 19mins)

This is a little longer piece at at 20 minute read, but you can choose to listen to my post by clicking the link here below.

Let me be upfront about something. I try hard in this newsletter to stay above the political fray — my job is to read markets, manage risk, and call things as I see them. But I’d be lying if I said I sit neatly in the middle. I lean right. I believe in markets, in property rights, in the idea that if you take risk and build wealth, the government shouldn’t be waiting at the finish line with its hand out. So read what follows with that lens in mind — and then ask yourself whether the numbers stack up regardless of your politics.

There is a wealth divide opening up in this country that nobody in Canberra wants to talk about honestly. It runs roughly along the age of fifty. On one side — the over 50s — a generation that built wealth through two of the most powerful tailwinds in modern economic history: thirty years of rising property prices and thirty years of falling interest rates. They got in early, they leveraged up, and the system rewarded them handsomely. Their assets are grandfathered. Their CGT discount is locked in. Their negatively geared properties — bought before budget night — are protected.

On the other side — the under 40s — a generation that missed the property boom, is now priced out of it entirely, turned to the share market and long-term investing as the alternative path to wealth, and has just been told that path is also going to cost them significantly more. New CGT rules. Negative gearing restricted on any new property they might buy. A two-trillion-dollar public debt loaded onto their future tax bills. And a government telling them this is all being done in their name.

The ability of the under 40s to build meaningful, compounding wealth across their working lives has been structurally impaired by this budget — while the over 50s who already hold the assets sit largely untouched. That is not an accident. It is the arithmetic of a government that knows exactly which cohort votes in higher numbers, and governs accordingly.

It’s Not A Lie If You Believe It

Because here’s the thing about this budget. Jim Chalmers wants you to believe it’s about intergenerational equity. About giving younger Australians a fair go. About levelling the playing field between those who earn wages and those who own assets. That’s a noble story. It’s also largely a fiction. What this budget actually is — stripped of the language and the spin — is one of the most significant tax grabs on investor wealth Australia has seen in a two generations, dressed in the language of fairness to make it politically palatable.

Oh — and before we go any further — let’s not forget that this same government, before the last election, looked Australians square in the eye and explicitly ruled out any changes to capital gains tax and negative gearing. Categorically. No ambiguity. Not on the table. You can go back and read the quotes. Anthony Albanese and Jim Chalmers were asked directly, repeatedly, and they said no. Then they won the election. Then they did exactly the opposite.

But I’m sure that’s just a coincidence. Perfectly normal to campaign on a promise, win government, and then do precisely what you said you wouldn’t. As George Costanza once told Jerry: “It’s not a lie if you believe it.” Apparently that philosophy now extends to election policy platforms. I’m sure voters will barely notice.

Let’s work through what they actually delivered.

The Tax Relief Is Real. The Maths Is Not.

Yes, working Australians get a tax cut. From 1 July 2026, the rate on income between $18,201 and $45,000 drops from 16% to 15% — worth up to $268 a year. By 2027, another cut to 14%, adding another $268. Plus a $250 Working Australians Tax Offset. Grand total by 2027: up to $536 a year extra in your pocket. That’s $10.30 a week. Enjoy your extra coffee.

Meanwhile, against an $833.2 billion spending budget and a $28.3 billion deficit, the government is quietly reaching into the pockets of every investor, property owner, and family trust in the country. The tax cuts are the headline. The revenue measures are the substance.

And before we go any further, let’s put that deficit in its proper historical context — because this is the number that should make every Australian furious regardless of their politics.

In 2004, Australia had no net federal government debt. None. In fact, under Treasurer Peter Costello, the Commonwealth had accumulated net assets — the nation’s balance sheet was in the black. Australia was the envy of the developed world for its fiscal discipline. The Future Fund was being seeded. Surpluses were being banked. The cupboard wasn’t just full — it had a surplus.

Then came the GFC stimulus. Then the NDIS. Then the pandemic. Then infrastructure blowouts, cost overruns, and a decade of governments from both sides of politics that discovered it is politically easy to spend and politically painful to stop. Each budget cycle added another layer. Each crisis became a reason to borrow more. And the interest bill — quietly, relentlessly — kept compounding.

Twenty-two years later, we are approaching one trillion dollars in federal government debt. From zero to a trillion in two decades. And this budget adds another $28.3 billion to that pile — in a year when the government is simultaneously telling Australians it is making the system fairer.

The CGT Reform: Not About Fairness — It’s About Revenue

This is where I want to spend real time, because it’s being sold as a fairer system — and it is anything but.

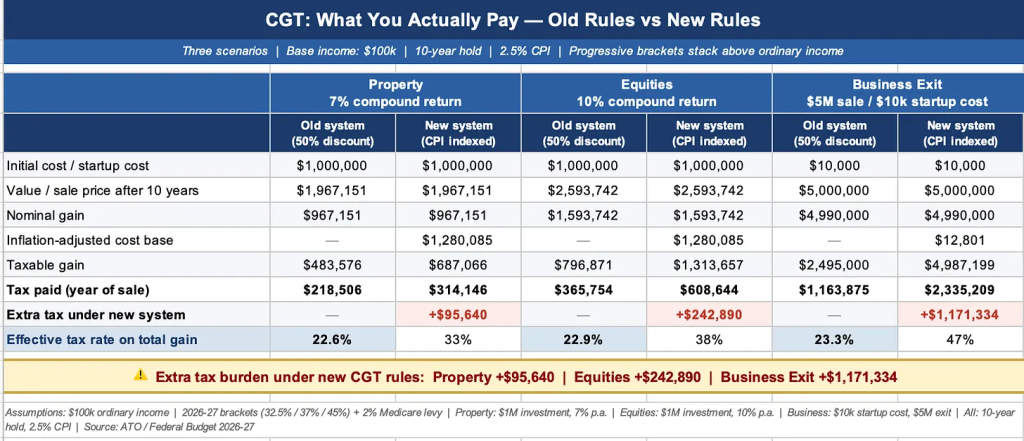

Under the current rules, hold an asset for more than 12 months — an investment property, a share portfolio, or a business you spent a decade building from nothing — and you pay capital gains tax on only half the nominal gain. The 50% discount. A rough-but-reasonable acknowledgment that some of what looks like a gain is simply inflation dressed up as wealth.

From 1 July 2027, for new investments and new businesses, the discount disappears. Instead, your cost base is adjusted for inflation and you pay tax on the ‘real’ gain above CPI. And here’s the kicker: a minimum 30% tax applies to all gains. No exceptions. Not for the retiree. Not for the ETF investor. Not for the founder who paid themselves half what they were worth for a decade.

Sounds fairer on the surface. The numbers tell a very different story.

The investor. On a $1 million property investment held for ten years, the new system hits you with an extra $95,640 in tax. On equities returning 10% over the same decade, an extra $242,890. Not a small adjustment. Not a technical tweak. A quarter of a million dollars extracted from someone who invested patiently, compounded responsibly, and did everything they were told to do. Your effective tax rate on the total gain jumps from 22.6% to 32.5% on property. On equities, from 22.9% to 38.2%. On the same nominal gain. On the same decade of patience. Just under a different set of rules.

The founder. Now let’s talk about the scenario no one is discussing. You start a business from scratch. Minimal capital — call it $10,000 to get the doors open. You pay yourself below market rate for years. You absorb risk that no corporate employee ever absorbs. Ten years later you’ve built something real, and you sell it for $5 million.

Under the old rules, your taxable gain is half of the $4.99 million nominal gain. Combined with $100,000 in ordinary income, your tax bill lands at approximately $1.16 million. Enormous — but proportionate to a decade of risk and sacrifice.

Under the new system, the government’s inflation indexing adjusts your $10,000 cost base to $12,800 after ten years at 2.5% CPI. That’s their concession for a decade of inflation: $2,800. Against a $5 million exit. Your taxable gain is now $4.99 million, taxed at full marginal rates all the way up. Your bill: $2.34 million. That is an extra $1.17 million handed to the government — on money that was never a salary, never a bonus, never passive income. It was the return on a decade of concentrated personal risk.

That is not a tax on wealth. That is a tax on entrepreneurship.

The concentrated winner. It gets decisively worse the moment you have a high-conviction call that pays off. Say you put $100,000 into a smaller company — three years later it’s done a 5x. Your $400,000 gain under the old rules costs you $85,225 in tax. Painful, but a fair reward for the risk you absorbed.

Under the new system, three years of 2.5% CPI indexing adds $7,689 to your cost base. That’s it. So instead of paying tax on $200,000, you’re paying on $392,311 — and your bill more than doubles to $175,611. A 44% effective tax rate on a three-year hold. An extra $90,386 to the government on a single position.

What connects all three? The 50% discount wasn’t generosity — it was imprecise but directionally honest. It said that real wealth creation deserves different treatment from ordinary income. The new indexing system, in theory, tries to do the same. But it fails completely in every scenario where the hold is short, the return is high, or the asset started from almost nothing.

The founder who built from $10,000 to $5 million gets almost no benefit from CPI indexing — $2,800 on a $5 million exit. The investor who backed a 5x in three years gets almost no benefit. The concentrated position holder gets almost no benefit. The only person the new system genuinely protects is someone who held a moderate-return asset across thirty years of elevated inflation — a scenario that describes almost no one investing today.

Everyone else pays more. Often substantially more.

And that’s not one investment. Not one business. Multiply it across an entire generation who opened their first brokerage account, launched their first venture, took their first real financial risk — and did exactly what every mentor, educator, and financial planner in the country told them to do. Every one of those decisions, made from 1 July 2027 onward, now carries this new tax burden. Not for the wealthy investor with the family trust and the tax adviser. For the 34-year-old founder with a cap table and a dream.

That’s not intergenerational equity. That’s the exact opposite.

How do we compare globally?

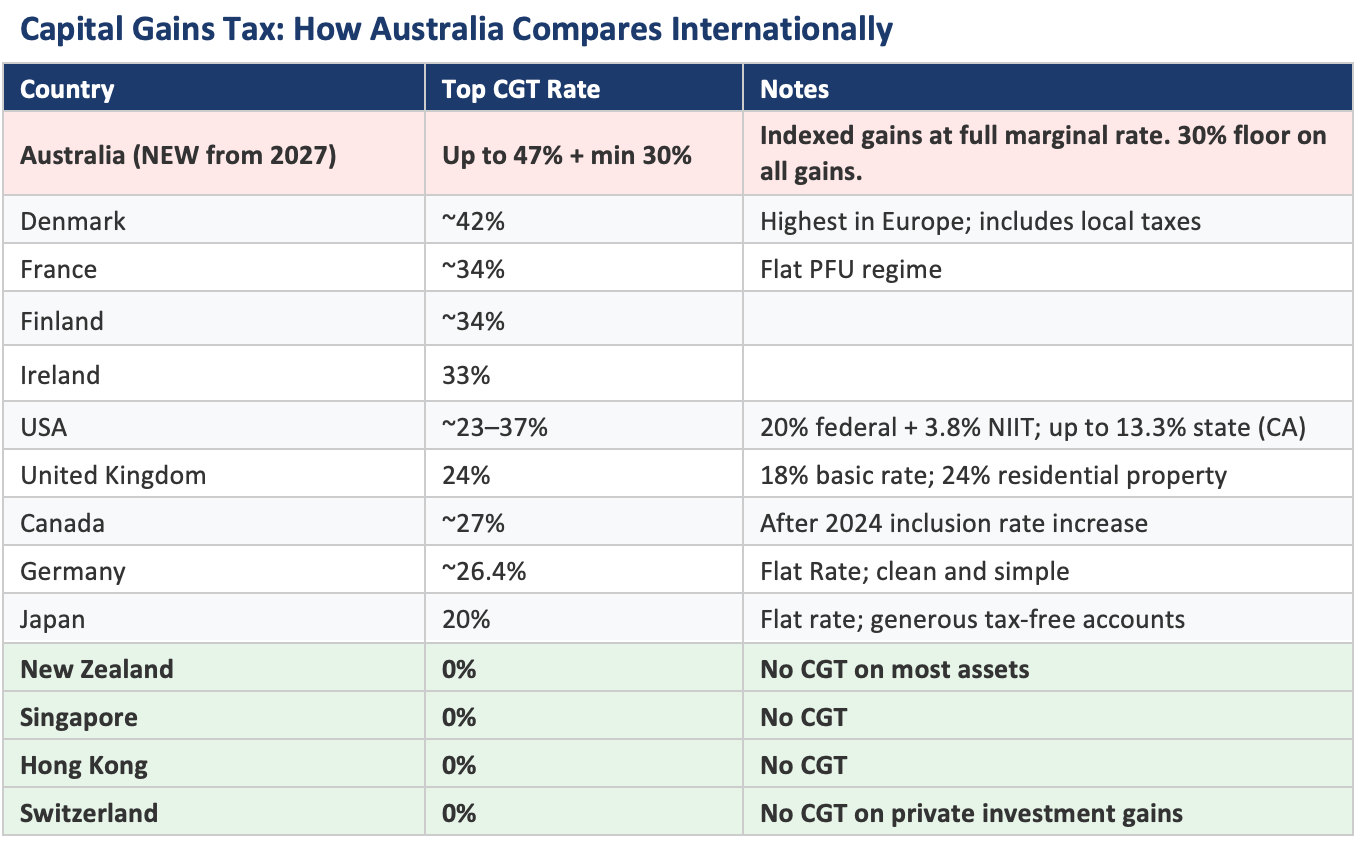

And before anyone argues Australia is simply aligning with global norms — let’s be very clear about where we actually stand.

Look at that table and let it sink in.

The countries that have built the great modern investment hubs — Singapore, Hong Kong, Switzerland, New Zealand — charge their investors zero capital gains tax. Not a lower rate. Not a discount. Zero. They made a deliberate decision that attracting capital, rewarding risk, and building long-term wealth were worth more to their economies than the short-term revenue of taxing investment gains. And it worked. Those economies are thriving, their capital markets are deep, and their wealthy residents aren’t leaving.

Now look at where Australia sits. Up to 47% plus a mandatory 30% floor. Above Denmark. Above France. Above the United States, the United Kingdom, Germany, and Japan — every country we actually benchmark ourselves against in economic policy. Not slightly above. Materially above. We have just positioned ourselves as one of the most punishing environments for individual investors in the developed world — at precisely the moment global capital has never been more mobile, and high-net-worth individuals have never had more choices about where to live, invest, and build wealth. This is not aligning with global norms. It is moving directly against them.

And the direction of travel couldn’t be clearer. A few hundred dollars a year back in your pocket from the income tax cut. Tens of thousands extra extracted over an investment lifetime from the CGT changes. The government gives with one hand and takes back — at ten times the scale — with the other. Any investor paying attention knows which hand did the real work on budget night.

Housing: Fixing Supply With a Policy That Ignores Supply

The crisis is not complicated: not enough homes relative to the people who need them. Australia added 450,000 people in the year to March 2025 alone — three quarters from net overseas migration. Over the next three years, roughly one million more arrive. Sydney’s median house price already sits at fourteen times median household income.

So what does Labor do? It restricts negative gearing on established properties — touching neither the demand side nor the immigration intake. If you wanted to design a policy that does nothing to solve a supply problem while appearing to do something for renters on social media, this is it. A $2 billion housing infrastructure fund is also announced — a positive step, but one that barely registers against a structural undersupply of this scale.

Then buried in Treasury’s own modelling comes the number that exposes the entire exercise. The government’s forecast for what all of this delivers on house prices: a 2% decline. Sydney’s median at $1.4 million drops to $1.372 million. Your deposit hurdle falls from $280,000 to $274,400. I’m sure the Millennial renter saving for a decade will be thrilled.

And the supply number is worse. Treasury’s own modelling projects these changes will deliver 75,000 additional homes over ten years — 7,500 a year. Australia needs roughly 400,000 new dwellings every three years just to house the people arriving from overseas. The government’s signature housing policy covers less than 6% of the demand its own immigration settings are creating. Sydney alone needs more than 7,500 new homes annually just to stop the deficit getting worse. This isn’t a housing policy. It’s a press release.

Negative Gearing: A Gift to Wealthy Investors, A Blow to Everyone Else

From 1 July 2027, losses on established investment properties can no longer be offset against wages or salary — only against rental income from other properties or capital gains. New builds remain fully deductible against all income. And if you already own an established investment property as of budget night — 12 May 2026 — you’re grandfathered. The old rules apply to you indefinitely.

Let that land. Every investor already in keeps the full tax advantage. Every investor trying to build wealth from here gets the new rules. This budget draws a clean line between those who already have assets and those still trying to acquire them — and calls it reform.

The policy intent is transparent: push investor demand toward new construction, add supply.

Catastrophically flawed in practice — and not for the reason most people are talking about.

New builds are now the only properties in Australia that can be negatively geared against salary income — the single most tax-advantaged asset class available. And who has the capital, the borrowing power, and the advisers to move fast on a new development? Wealthy investors. Not first home buyers. Not young couples saving a deposit. So the government has created a land grab and handed the flag to the people least in need of the advantage.

These investors won’t just win on the tax break. They’ll win twice. The established market — where the vast majority of rental stock lives — becomes increasingly constrained. Fewer investors, fewer rentals, less supply, higher rents. The wealthy new build investor collects the tax deduction on one side and rising rental income on the other. A government-engineered double benefit, extracted from a market the policy itself tightened.

And the first home buyer — the supposed beneficiary — is now competing with those same wealthy investors for the only tax-advantaged stock left. Let’s be clear about where that stock actually is: outer suburb land releases, growth corridors an hour from the CBD, where young families were already being pushed by affordability. And what did new house and land prices do the moment this policy was announced? They went up. Overnight. Give it a month or two and you’ll read it on the news — new build prices surge post-budget. The young family this policy was designed to help just watched their only option get more expensive before the ink was dry.

We have been here before

Negative Gearing changes, well we’ve done this before. Exactly this. In 1985, Paul Keating — same party, same instinct — quarantined negative gearing in almost identical fashion. The result? Sydney and Perth rents spiked double digits within two years. The Hawke government reversed the policy completely in 1987. Less than two years it was gone.

Today’s national vacancy rate is as tight as 1985 Sydney — everywhere, not just two cities. The damage this time won’t be concentrated in two cities. It will be national, and it will fall hardest on the renters and first home buyers who were told this policy was designed for them.

Family Trusts: Another Quiet Revenue Measure

From 2028-29, distributions from discretionary (family) trusts face a minimum 30% tax rate — closing the long-standing income-splitting strategy where trust income was distributed to lower-income family members.

There is a three-year restructure window from July 2027. If you operate through a family trust, the time to call your adviser is now — not next year, not when the rules come in. Now. This one has teeth and the window to restructure is finite.

When you have that conversation, make sure it’s a real one. Ask your accountant or financial adviser to model what a restructure actually looks like for your specific situation. The structure that served you well for the last twenty years may not be the right structure for the next twenty.

One alternative that deserves serious consideration: the investment company. A company structure pays a flat 25–30% corporate tax rate, retains earnings at that rate, and doesn’t carry the same income-splitting vulnerabilities. Franking credits still flow to shareholders on dividends. It’s not a perfect substitute — there maybe CGT implications in restructuring and the tax on dividends as you realise your capital in you own hands— but the investment company model may well replace the family trust as the preferred vehicle going forward.

The Generation That Got Robbed Twice

I want to say something directly to the Millennials and Gen Z reading this — because this is the part that makes me genuinely angry.

You were told the path to wealth was property. Then prices ran so far ahead of wages that the deposit became a decade-long savings marathon — not through laziness, not through avocado toast, but through a straightforward mismatch between asset prices and income growth that no amount of sacrifice could close. You were locked out. So you adapted. You turned to shares, ETFs, managed funds, long-term investing in the market. You did exactly what every financial educator, every wealth adviser, every self-help book told you to do. You took responsibility for your own future.

And this budget just changed the rules on that too.

From 1 July 2027, every new investment you make will cost you significantly more when you eventually sell. The table earlier in this post shows you exactly how much more. Read it again if you need to — because those numbers represent your money, your future, your decade of patience. The rules changed. After you sat down at the table.

That is not intergenerational equity. That is the exact opposite of it.

And then there’s the bill waiting at the other end of your working life. Australia’s Commonwealth debt is on track to exceed one trillion dollars within the next year — money that has to be serviced, managed, and ultimately repaid by the same generation that was locked out of property and is now taxed harder on every alternative they turned to. And the federal figure alone understates the true burden. Every state carries its own debt, implicitly backed by Canberra. Victoria alone sits above $170 billion. New South Wales not far behind. Consolidate federal and state and the number doesn’t approach one trillion — it approaches two trillion dollars. That is the real intergenerational balance sheet. Not the tidy figure Jim Chalmers presents on budget night.

And here’s the part nobody questioned hard enough. The government is forecasting inflation to fall from around 5% to 2.5% — smoothly, tidily, right on cue. Let me remind you when Australia last saw 2.5% inflation. Pre-COVID. 2019. We have not been at 2.5% since then — and there is no credible mechanism that gets us back there while the government is running a $28.3 billion deficit and adding a million people every three years.

Inflation is sticky. It doesn’t respond to wishful thinking in budget papers. Every percentage point above forecast means rates stay higher, debt servicing blows out, and the choice is more borrowing, deeper cuts, or higher taxes. The fiscal arithmetic only works if the inflation forecast is right. And the inflation forecast is not right.

The Boomers and Gen X built wealth in an era of falling rates, rising asset prices, and tax settings that rewarded investment. That era is over. The generation inheriting what comes next is being asked to fund the bill for a spending regime they had no say in creating. And the government is calling this intergenerational equity.!

I’ve spent 37 years in financial markets. I’ve seen a lot of spin. But rebranding a trillion-dollar debt burden and a structural tax increase on younger investors as fairness — that takes a particular kind of audacity.

A Personal Note — And a Call to Action

I want to step back for a moment, because I’m aware this has been a relentless piece of writing. Pessimistic, critical, at times angry. And I want to be honest about why.

It’s not because I’m doing it tough. I’m in my mid-fifties. I’ve had 37 years in financial markets. I’ve built what I’ve built, and I’m genuinely grateful for it. This budget doesn’t keep me up at night — not personally. I’ll adapt, restructure where I need to, and get on with it.

But I have two children in their twenties. And when I look at what this budget means for them — for their generation — I feel something that goes well beyond frustration at poor policy. I feel genuine concern.

My parents’ generation bought homes on a single income. My generation stretched to get in — but we got in, and the market did the rest. My children’s generation is being asked to build wealth with one hand tied behind their back. Priced out of property. Now taxed harder on every alternative. And left to pick up the tab for two trillion dollars of public debt they had no hand in creating.

So yes — I lean right. But this isn’t really a left versus right argument anymore. This is about whether you believe younger Australians deserve the same opportunity to build wealth that every generation before them had. I do. Deeply.

Millennials and Gen Z together now represent the largest voting bloc in this country. Larger than the Boomers. Larger than Gen X. If that generation votes — really votes, with intention and understanding — governments will listen. They always do when the arithmetic forces them to.

I’m not here to tell you who to vote for. That’s genuinely not my place. But I am asking you to vote with your eyes open. To look at what this budget actually delivers for your future — not the headline, not the spin, not the $10 a week tax cut — and decide whether the people who made these decisions are giving you the same opporunity your parents and grandparents received.

Postscript Imricor Medical : The One Stock This Budget Doesn’t Change My Mind On

I believe in what Imricor is building — genuinely, not as a footnote. This is technology that helps human beings. The ability to perform cardiac procedures inside an MRI scanner — real-time, live imaging, no radiation — is not an incremental improvement on what came before. It’s a fundamental rethinking of how we treat the heart. And when you extend that into paediatric cardiology — children born with structural heart conditions who can least afford the cumulative radiation exposure of conventional procedures — the case for this technology stops being financial and becomes something more important. The fact that it’s also a compelling investment is almost secondary to what it actually does. I’ve held since around 30 cents and haven’t sold a share — and that’s not stubbornness. It’s conviction.

Recently the company completed a A$60 million capital raise and is now fully funded well into 2028. For early-stage medical technology companies, running out of cash at the wrong moment is the single most brutal risk — it has killed businesses far better than this one. That risk is now off the table.

When you’re funded, you stop having existential conversations and start having commercial ones. Hospital procurement teams don’t commit to multi-year technology decisions with companies they’re not sure will be around. Funding certainty unlocks conversations that couldn’t happen before. In MedTech, that matters enormously.

What makes this raise particularly compelling is the timing. Imricor isn’t raising capital hoping something will eventually work. The core technology is proven, key products are approved in Europe, the NorthStar mapping system is cleared for US commercial launch, and the sales pipeline is rebuilding. The scientific and regulatory groundwork has been laid. The money is now there to commercialise it.

The business model is straightforward and powerful. Once a hospital installs an iCMR lab, two revenue streams follow — upfront equipment sales and ongoing consumable catheter sales for every procedure thereafter. At roughly 500 procedures per year per lab, a single hospital becomes a multi-million dollar recurring revenue customer. Revenue that builds, compounds, and sticks.

Imricor today is not the same company it was twelve months ago. The technology works. Regulators are engaged. Customers are committing. The company is now properly capitalised to execute without distraction. Execution risk remains — it always does in MedTech. But the risk that ends companies early? Gone. That’s a meaningful shift — and the broader market is starting to recognise it. Taylor Collison recently lifted their 12-month price target to $3.45, a level that reflects a more realistic view of what this business is capable of as it moves from development into commercialisation. I don’t think even that fully captures what this looks like in three to five years if the US launch gains traction.

That’s The GoodFellas Way for this week. If this resonated — share it with someone who needs to hear it. Subscribe if you haven’t already. And if you disagree with any of it — I genuinely want to hear from you. The best thinking is stress-tested thinking.

Until next time — stay sharp, stay patient, and protect your capital