Payday Super | CGT Reform | Negative Gearing | Trust Tax | Xero Pricing

The Federal Budget delivered on 12 May 2026 reshapes the rules around capital gains, property investment, and family trusts — changes material enough to affect how you invest, structure, and plan. Payday super also kicks in from 1 July, tightening payroll obligations for every employer.

Here’s what you need to know.

1. Personal Income Tax Cuts

Every working Australian receives a tax cut from 1 July 2026. The rate on income between $18,201 and $45,000 drops from 16% to 15%, with a further reduction to 14% from 1 July 2027. A new $1,000 instant work expense deduction also applies from 2026–27, removing the need to hold receipts for standard work-related claims — a practical win for most employees.

2. Capital Gains Tax Reform — A Material Shift for Investors

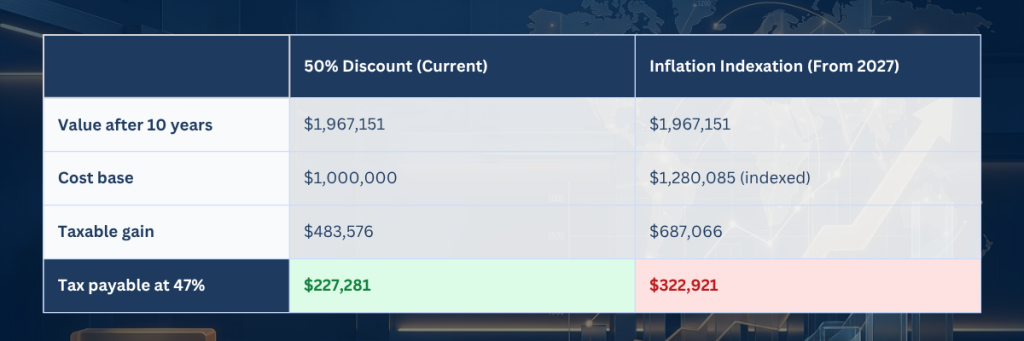

This is one of the most significant changes in the Budget. From 1 July 2027, the 50% CGT discount for assets held longer than 12 months will be replaced by inflation indexation.

Assets acquired before 7:30pm AEST on 12 May 2026 are grandfathered under the existing rules and retain the 50% discount.

What this means in practice:

The numbers tell the story clearly. Take a $1 million investment held for 10 years, growing at 7% per annum with inflation at 2.5%:

The difference: $95,640 more tax under the new regime — on the same investment, with the same return.

For investors holding appreciating assets — property, shares, managed funds — this is a material change that should be factored into any future acquisition or disposal decision. If you hold or are planning to acquire investment assets, speak with your adviser before acting.

3. Negative Gearing — New Builds Only

From 1 July 2027, negative gearing deductions will be limited to newly constructed residential properties. Existing investment properties are grandfathered — if you already own an established investment property, your deductions are preserved.

For investors considering future property purchases, this changes the equation meaningfully. Established properties purchased after the cutoff will no longer generate deductible losses against other income. New builds, off-the-plan, and house-and-land packages become the primary vehicle for property investors seeking negative gearing benefits.

4. Discretionary Trust Minimum Tax

From 2028–29, a minimum 30% tax rate will apply to discretionary trust distributions. This fundamentally changes the income-splitting strategy that family trusts have long relied upon.

Previously, distributions to low-income beneficiaries — adult children, non-working spouses, or other family members — were taxed at their lower marginal rates, reducing the overall family tax burden. Under the new rules, all distributions will be subject to at least 30% tax regardless of the beneficiary’s personal income.

What this means in practice:

The income-splitting benefit of a family trust is largely eliminated for distributions to beneficiaries earning below $120,000. For families where the primary purpose of the trust was to distribute to lower-income members, the compliance cost and administrative burden of maintaining the structure may now outweigh the tax benefit. Trusts retain their appeal where beneficiaries are on higher marginal rates of 37% or 45%, but the calculus has changed significantly.

We recommend a review of your trust structure before 2028–29 if you are currently distributing to lower-income beneficiaries.

5. Payday Super — Effective 1 July 2026

From 1 July 2026, employers must pay superannuation with every pay run — not quarterly. Contributions must reach the fund within 7 business days of each payroll date.

Key employer obligations:

- Super is calculated and remitted each pay cycle, in line with wages

- Quarterly lump-sum payments are no longer permitted

- Late or missed payments will trigger the Super Guarantee Charge (SGC), which is not tax-deductible

Three areas to address before July:

- Cash Flow — Payments shift from quarterly to frequent outflows. Review your forecasting to ensure funds are available each pay cycle without disrupting operations.

- Systems — Your payroll platform must be configured to calculate and remit super automatically at each pay run. Manual processes carry real compliance risk under the new regime.

- Compliance — The SGC penalty applies from day one. If your current processes rely on quarterly reconciliation, update them now.

Recommended steps:

- Confirm your payroll system supports automated payday super

- Update HR and finance workflows

- Revise cash flow forecasts to reflect more frequent super outflows

- Brief your employees on the change ahead of July

Our fees: In line with these changes and consistent with current inflation, we will also be applying a 4% increase to our fees from 1 July 2026.

Direct Debit Discount: Clients who elect to pay by direct debit will receive a 2% discount on our fees, applied automatically. This makes credit card payments effectively fee-free — no surcharge, no additional cost — while rewarding those who choose the convenience of auto-pay. To set up direct debit or discuss the fee changes, please get in touch.

Several of the Budget changes — particularly CGT reform, negative gearing, and trust taxation — are complex enough that the right course of action depends on your individual circumstances.

If you’d like to discuss what these changes mean for you specifically, please reach out to your adviser. We’re here to help you navigate them.

Want to know more about the impact of this budget? Read Chris’ note here: https://goodfellasinvesting.substack.com/p/australians-under-40s-just-got-roggered?r=1lbdvn